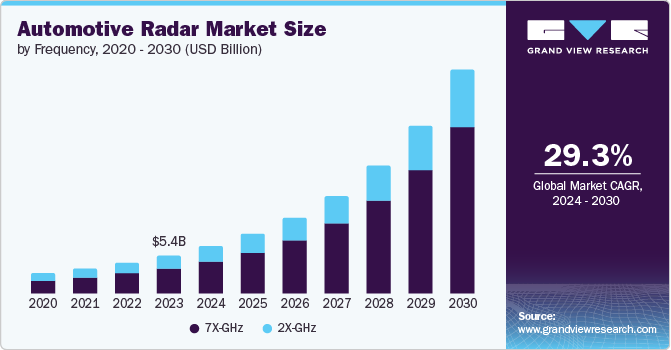

The global automotive radar market was valued at approximately USD 5.40 billion in 2023 and is projected to reach USD 31.45 billion by 2030, growing at a compound annual growth rate (CAGR) of 29.3% from 2024 to 2030. The increasing emphasis on passenger safety due to the rise in accidents worldwide is driving this growth. According to a WHO report, around 1.19 million people die annually due to road traffic crashes, prompting governments to enforce stricter safety regulations aimed at protecting passengers and enhancing the overall driving environment.

Modern vehicles utilize various radio frequency devices to improve safety while driving. The rising demand for Advanced Driver Assistance Systems (ADAS) is a significant factor, as radar technology is crucial for functions such as parking assistance, adaptive cruise control, blind spot detection, and autonomous emergency braking. High-end vehicles often feature pilot modes and driver assistance modules, where a central computing system employs radars, actuators, and sensors to assist in driving tasks. Automotive radars provide accurate information on object tracking, detection, and motion prediction, thereby enhancing the quality of automated driving.

The development of self-driving vehicles is heavily reliant on radar systems for detecting, measuring distances, and tracking objects, which further propels market growth. Additionally, advancements in technology that improve radar performance, reduce size, and lower costs are increasing the feasibility of integrating radar into a wider array of vehicles. Growing consumer awareness regarding vehicle safety and a preference for high-tech features also contribute to the market's expansion.

Order a free sample PDF of the Automotive Radar Market Intelligence Study, published by Grand View Research.

Key Market Trends & Insights

- The Europe automotive radar market dominated in 2023, accounting for 36.02% of the total market share. This substantial growth is primarily due to governmental efforts in the UK, Germany, and other European nations to promote safe transportation. Additionally, stringent safety regulations are increasing the demand for ADAS.

- By range, the medium and short-range radar segment led the market with a share of 54.9% in 2023 and is expected to register the fastest CAGR of 30.3% during the forecast period. The rise of technologies such as rear cross-traffic alert, adaptive cruise control (ACC), heading distance indicators, and autonomous emergency braking (AEB) is driving growth in this segment.

- In terms of frequency, the 7X-GHz segment accounted for the largest market revenue share in 2023 and is expected to exhibit the fastest CAGR during the forecast period due to its high accuracy in detecting objects and its ability to operate in various weather conditions. Radars operating at this frequency are used for short-range applications, including adaptive cruise control, collision alert, and lane departure warnings.

- By engine type, the internal combustion engine (ICE) segment dominated the market in 2023, owing to its significant presence across the automotive sector. Despite the rapid growth of the electric vehicle (EV) market, ICE vehicles still constitute the majority of vehicles on the road, presenting substantial opportunities for radar technology integration.

- In terms of application, the adaptive cruise control (ACC) segment led the market in 2023. Stringent government regulations are expected to boost the demand for ACC, which adjusts vehicle speed based on nearby vehicles. Radar systems located at the front of a vehicle detect the speed of vehicles ahead and adjust the vehicle's speed accordingly.

- By vehicle type, the commercial vehicles segment dominated the market in 2023. The increased risk of accidents involving large commercial vehicles underscores the need for advanced safety measures. Radar technology is essential for enhancing road safety, minimizing injuries, and preventing crashes in commercial vehicles.

Market Size & Forecast

- 2023 Market Size: USD 5.40 Billion

- 2030 Projected Market Size: USD 31.45 Billion

- CAGR (2024-2030): 29.3%

- Europe: Largest market in 2023

Key Companies & Market Share Insights

Key players in the automotive radar market include ZF Friedrichshafen AG, Robert Bosch GmbH, HELLA GmbH & Co. KGaA, Denso Corporation, and others. These organizations are focusing on expanding their customer bases to gain a competitive edge in the industry. Consequently, major players are undertaking strategic initiatives such as mergers, acquisitions, and partnerships.

- Valeo, a prominent automotive technology company, is known for its radar systems. Their product range includes mid-range radar sensors for ADAS and automated parking, high-definition radar sensors for advanced driver assistance and automated driving, and parking assistance systems, catering to various vehicle types and incorporating the latest technological advancements.

Key Players

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Valeo

- ZF Friedrichshafen AG

- HELLA GmbH & Co. KGaA

- Autoliv Inc.

- Infineon Technologies AG

- Texas Instruments Incorporated

- NXP Semiconductors

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The automotive radar market is poised for substantial growth, fueled by the increasing focus on passenger safety and the rising demand for advanced driver assistance systems. With stringent safety regulations and the development of self-driving vehicles, radar technology is becoming essential in enhancing road safety and improving the driving experience. As the market evolves, advancements in radar technology will likely lead to broader integration into various vehicle types, driving further growth and innovation in the automotive sector.